Introduction

The recent crash of the Crypto market led to a cascade of events which had several crypto lending platforms in the worst liquidity crisis ever seen in the market. In a bid to prevent complete dissolution, various platforms took extreme measures by pausing all withdrawals, swaps, and transfers. This act increased panic and exacerbated the situation; causing further devaluation of key tokens in the crypto market, leaving lending platforms unable to repay loans/meet margin calls.

Though most of this could have been avoided if investors simply heeded to expert advice, the chance for an attractive APR blinded users to the high-risk vulnerabilities of crypto lending platforms.

Following such an incident, the wise investor is to be found seeking answers as to How Crypto Lending works, its risks, and vulnerabilities. This article attempts to provide a sufficient education on Crypto loans and their attractive, yet deceptive nature.

What are Crypto Loans and How Do They Work?

The lending system in the Crypto space is almost identical to its traditional market alternative, with the only difference being the use of crypto assets, and complete discretion of usage. Instead of storing cryptocurrencies in your wallet, Crypto lending platforms offer attractive interest rates for choosing to store your assets with them, these stored assets are then loaned out with interest which the platform makes its profits from.

Players in Crypto Loans

(i) Those seeking to increase their portfolio via a passive income by depositing assets to be used for loans.

(ii) Those using crypto assets as collateral to take out loans.

(iii) The platform hosting both parties.

The process:

- The host platform attracts investors to deposit their crypto for good APR (annual percentage rate.)

- The borrower approaches the host platform for a loan.

- He then stakes some of his crypto assets as collateral against the requested loan.

- The host platform uses the initial investors’ deposits to fund this loan and holds on to the borrower’s staked assets until he repays the loan in full.

- The host platform makes profit in interest when the loan is repaid, and investors earn yields on deposits.

Types of Crypto Lending Platforms

-

CeFi Platforms

Centralized finance (CeFi), is used to describe platforms in the crypto market which act as a third party, overseeing all transactions on their platform. They do this by managing exchanges, swaps, transfers, and by ensuring users are well-identified using KYC tools. In the lending space, they bring both borrowers and lenders together, helping manage lending processes. Such platforms include, BlockFi, Celsius, Gemini, 3AC, Babel, etc.

-

DeFi Platforms

Decentralized Finance (DeFi) describes financial institutions in the crypto market without any governing body or central authorities overseeing transactions. These platforms make use of smart contracts which self-executes when all conditions have been fully met. For transparency, these contracts are often made available for users to view and assess. In the lending space, they make use of liquidity pools to store assets to be made available for loans. Decentralized financial platforms include, MakerDAO, Compound, Aave, Pancakeswap, etc.

Types of crypto loans

Flash loans

Flash loans are a type of uncollateralized loan, meaning they don’t require a collateral to access. The term ‘Flash loans’ is given to them because they require immediate repayment, within the same block. Flash loans are used to quickly make profitable trades, if the trader makes a profit he pays a percentage fee from earnings, in case of a breakeven, the funds go back to the lender with interest.

Collateralized loans

These are traditional loans that require the deposit of an asset before loans can be accessed. This allows the borrower more time to use loaned funds. Collateralized loans can be paid in full or installments or by automatic liquidation. For example, on MakerDAO, if the value of a collateral decreases beyond a given point against the DAI borrowed, the collateral will be automatically liquidated to be used to repay borrowed DAI and additional fees. Such platforms offering these loans include BlockFi, Celsius and MakerDAO.

Crypto lending was welcomed for introducing a safe and secure means for investors to increase their portfolios but recently, core vulnerabilities of these platforms have been exposed. Although some of these vulnerabilities have for long been observed, the recent crypto market crash has only just brought them to light.

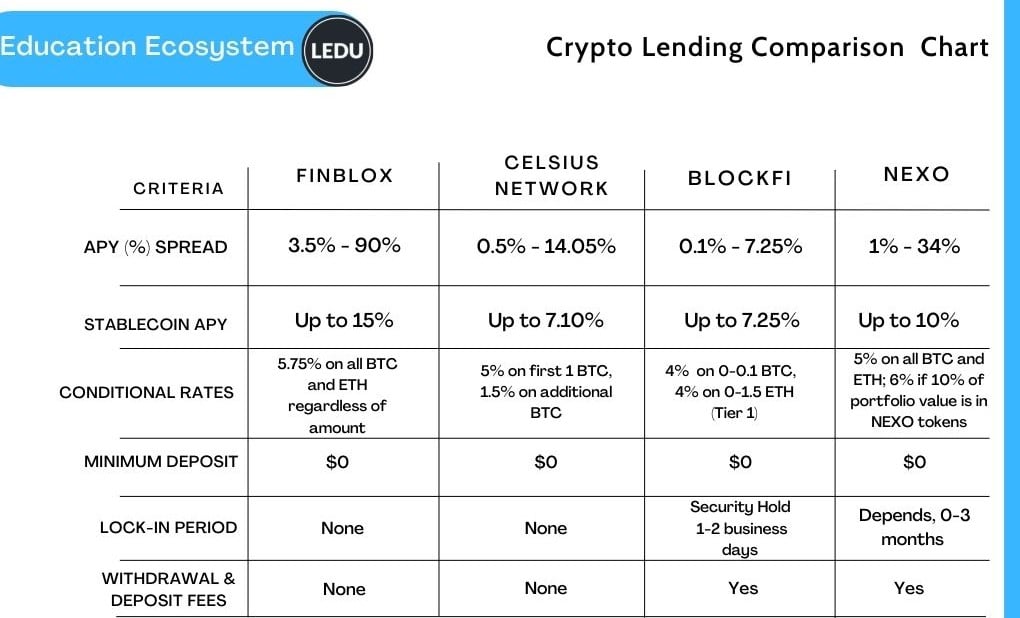

comparison of Crypto lending platforms discussed

Risks associated with Crypto Lending

Insolvency risks: What if the lending platform becomes broke?

In this risk we have another difference between the concept of lending in the traditional market and its application in the crypto market. In the traditional market, bank deposits are insured with the central finance authority against the possibility of liquidation of an institution; since the crypto space lacks a governing body, there is no third-party securing deposits (safeguarding investors). In the event of insolvency, which is a situation whereby the financial institution is unable to refund deposits back to investors, there is no form of insurance and investors end up losing all deposits.

Recently, several platforms were affected by this, particularly, Three Arrows Capital (3AC). Wrong management decisions led to 3AC losing around 60% of its investments. The platform spent $559.6m acquiring locked LUNA tokens, now worth around $700 after the crypto markets crashed. Sighting this, yield generator, Finblox made a swift move to set a cap on their withdrawals and paused all yield rewards.

Counterparty risks: How does the lending platform use your deposits?

Recall that lenders deposit assets for interests, and borrowers deposit assets for a loan, the third-party (host platform) is in possession of both assets. These platforms sometimes make money off deposits by lending them to an additional party over-the-counter.

Blockchain, a popular exchange is currently experiencing such after giving a $270m loan to Three Arrows Capital (3AC) currently facing liquidation. The latter is unable to repay loans, leaving blockchain with a massive loss.

Similarly, one of the largest lending platforms, Celsius, fell into this debacle after investing customer’s Ethereum deposits with Lido finance. Lido offered its customers a chance to profit from its new version of Ethereum, “Staked” Ether or stETH which was supposed to match the value of Ethereum, ratio 1:1. But following the recent market crash, the value of stETH plummeted, leaving Celsius unable to convert its stETH back to ETH to pay its customers. This emphasizes the importance of counterparty risks.

Security Concerns: How safe are my personal data and deposits?

The crypto space is replete with various incidents of hacks and theft, although no crypto lending platform has been a victim of asset theft, private data has been leaked in some incidents. Private keys together with deposits are in possession of a third-party (host platform) increasing the risk of a great loss if affected by a hack or theft. Some CeFi platforms like Gemini and NEXO are covering the risk of theft with private insurance policies.

Legal Infancy: Crypto regulations barely exist

With the slow adoption of cryptocurrencies globally, there are very few laws guiding the safety of its use and implementation. Hence, decentralized exchanges cannot be subjected to any laws. Since contracts don’t exist in the DeFi space or at least legally backed contracts, you can’t hold any party responsible for your losses.

Volatility: A major concern

This is a frequent concern that occurs in all facets of crypto, volatility. In crypto lending, volatility poses a major concern as returns could be worth less than their initial loaned value, leaving an investor with huge losses. As in the cases of 3AC and Celsius, in which due to the volatility of the crypto market, investments in other tokens were lost due to depreciation. Which left both platforms facing insolvency.

Conclusion

The crypto space is heavily associated with risks, some even call it the ‘Wild West’ as it appears to be a lawless space. With this knowledge, all investors ought to be aware of the constant risks associated with free-floating cryptocurrencies, even with custodial bodies, there’s only minimization of risks. There’s a common saying ‘If it’s too good to be true, it probably is.’ Crypto lending platforms used high APRs to lure investors without being able to back the generation of these interests. At the end, investors were rekt. Although, an in-depth research before any investments in this space is necessary, always keep in mind there will always be risks.